The extraordinary boom in the property market in Malaysia is ending but high house prices and the middle-class obsession with home ownership are likely to persist for a long time to come.

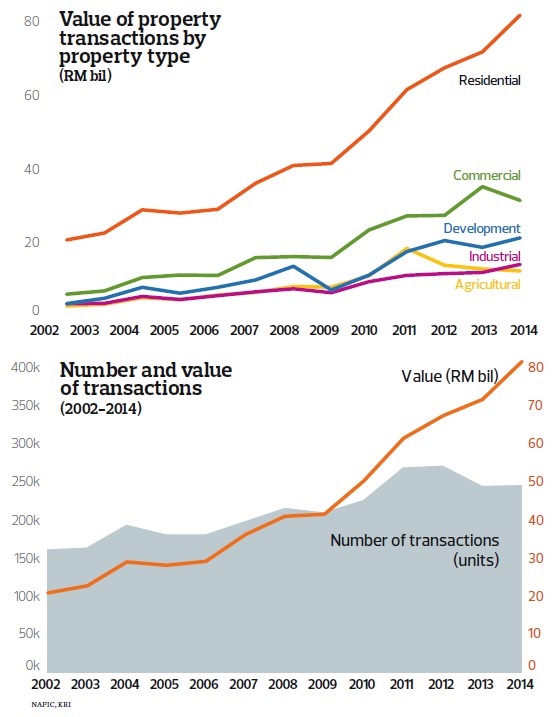

Data from the National Property Information Centre’s (Napic) First Half Property Market Report shows that during the first six months of the year, the total value of property transactions declined 6% year on year to RM77.08 billion. In terms of volume, property transactions fell 3.5% to 186,618. The residential segment saw a 2.6% drop in transaction volume but its value took a 9.7% dive to RM36.4 billion.

The report will make sobering reading for many younger households who, for years, have seen property prices only move northwards. Between 2009 and 2014, the Malaysian House Price Index registered a compound annual growth rate (CAGR) of 10.1%. It marked a period of sharp acceleration compared with 5.6% for the period between 2000 and 2014.

This rapid growth in an otherwise sedate domestic property sector came on the back of ample liquidity that flooded the market following the global financial crisis in 2008. Predictably, grumbles that houses were too expensive for the hardworking middle class emerged. The government attempted to halt this price growth by stopping free-flowing mortgages and stepping efforts to combat speculative activities as early as 2011. Price growth slowed but it was not till 2015 that growth in residential property deals stalled.

This year, property developers are struggling with sales. Few are selling or building properties at rates seen during the housing boom and Napic reported that property stock, which stood at 4.87 million units in 1Q2015, grew to 4.89 million units in 2Q2015. At the same time, new launches fell 12.8% in 1H2015 year on year while unsold units under construction rose a whopping 32.7%.

These unsold residential units have started to subtly drive prices down. Napic’s numbers indicate that as at 2Q2015, the Malaysian House Price Index was at 220.2 points, up 5.9% y-o-y. The rate of increase of the index has been slowing since 3Q2015.

“House prices have definitely come down. If you don’t see them, it is because property developers have started to offer rebates, discounts or other incentives like free legal fees or stamp duties, which will lower the amount you pay for the property in the end,” says Chang Kim Loong, secretary-general of the National House Buyers Association.

If the additional supply is helping to moderate property prices, then some will find Napic’s data on incoming supply comforting. It reported that Malaysia had incoming supply of 795,372 residential properties in 1Q2015, which increased to 831,186 in 2Q2015.

While private developers are more cautious about adding on to that, the government is not. Based on the 11th Malaysia Plan, the government, through various housing programmes, targets to deliver 653,000 new housing units from 2016 to 2020. The sum excludes many state housing schemes.

For the middle class in particular, the 1Malaysia People’s Housing (PR1MA) programme should be adding an extra half a million affordable homes by 2018. The bulk of the promised 500,000 units should enter the market in 2017 and 2018. Lest we forget, there is also the government’s directive to government-linked companies to build 800 units in Bandar Kwasa Damansara and for Sime Darby Property to build 4,600 units of affordable homes.

Also reassuring for aspiring homeowners is that those in the business of building homes are not expecting property prices to see a surge. They tell The Edge that growth in house prices is likely to stagnate in the near term, as buyers looking for new properties and prepared for the added debt burden are denied owing to lending restrictions.

Bina Puri Holdings Bhd executive director Matthew Tee says, “I expect property prices to remain at current levels, with growth capped by the current regulatory environment. I don’t see prices coming down too much because the cost of development is very high. Land and other costs are still going up.”

Ken Holdings Bhd’s Sam Tan says, “The property development business is not as easy as it used to be. You have to offer more amenities, and provide connectivity and infrastructure to attract buyers. Developers’ profit margins are thinning due to rising costs and slowing market.

“It depends on what you build and how you price your product. The bread-and-butter properties — those priced between RM300,000 and RM500,000 — will still sell. But, generally speaking, you will not see a surge in prices anytime soon.”

So, are moderating residential property prices arising from an increase in supply the answer to the housing affordability woes of the middle class?

MIDF Research economist Izzuddin Yusuf doesn’t believe that is the case. Property prices have swelled too much over the last few years for a small tapering off to count. Affordability is still an issue for most middle-income earners looking to live under their own roof.

“I think the idea of affordable housing has changed recently for the public, to a point that it is considered affordable so long as you are eligible for a bank loan.

“Property prices are currently at a level that is still unaffordable for ‘real demand’, meaning those who buy in order to live in the property, even as speculative buying has slowed significantly. From here, property prices will probably grow at a very slow pace and it will be a while before they become affordable for most first-time buyers,” he says.

Indeed, Khazanah Research Institute’s (KRI) study, “Making Housing Affordable”, found that the the median price for the Malaysian housing market exceeded the three times median annual household — the threshold for affordability. The general median price stood at4.4 times in 2014 — a seriously unaffordable level. In cities like Kuala Lumpur and Penang, residential properties were “severely unaffordable”. Launches were priced way above the affordable threshold of RM274,320 for the capital city and RM168,272 for Penang.

Implicit in KRI’s statistics is that house prices — soaring or moderating — is not the only variable that determines if a middle-class household can afford to buy a property. It also has to do with income level and growth in disposable income.

“Housing affordability is not simply about having cheaper houses … For a house to be affordable, it means that the purchaser has the budget to pay for the home,” says Teh Lip Kim, managing director of Selangor Dredging Bhd.

Ken Holdings’ Tan says, “We try to build affordable homes and what is being sought after, but people still have to be able to buy them. People are now in a situation where banks are tightening lending requirements. [They also] have one or more banking loans to service and face a higher cost of living.”

“To buy a property, you need the additional disposable income. While wages in Malaysia are growing and the employment rate is good, they are not growing as fast as property prices. The higher your income, the more affordable a house will be to you.”

Further, socially popular regulations that stifle property price growth may help quiet public complaints about housing affordability, but won’t do more than that for the Malaysian economy. Not only does the construction sector contribute directly to the country’s gross domestic product (GDP) but it also has a strong multiplier effect. As it also affects sectors like finance, building materials, logistics, infrastructure development and job creation, it is unlikely that a prolonged sluggishness in property prices is what the government wants.

Rajiv Biswas, chief economist at IHS, says, “The construction sector in Malaysia accounted for 4.3% of GDP in 2014, based on government data. Therefore, the size of the sector is significant and any significant slowdown would act as a drag on GDP growth.

“Therefore, if the private sector residential construction sector experiences a downturn, the overall impact on total construction activity could be reduced by stronger public sector spending on affordable housing and public infrastructure projects.” But even as growth in home prices is losing steam, the dream of home ownership may still remain elusive to the middle class. - By Yen Ne Foo / theedgeproperty.com

Malaysia Property News

- ▼ 2015 (308)

- ▼ November (57)

- Overcoming resistance to IBS

- REV.O office suites 95% taken up after launch

- GuocoLand’s upmarket Damansara City Mall 50% taken up

- Long-term solution needed to house the people

- Thriven Global Bhd to launch RM1.8 bil of projects

- Malton hits billion ringgit sales

- High demand for factory lots could push up space p...

- Waiting for cheer from GuocoLand’s divestments

- Kuala Lumpur soon to boom with mega projects

- 20,000 affordable homes to be built in Putrajaya

- Econpile wins RM95.5mil job in Mont Kiara

- Banks rejecting qualified first-time house buyers

- Your property of choice at the fair

- UOA net profit up on higher property sales

- I-Bhd unbilled property sales rise to RM680mil

- 1MDB RE: Bandar Malaysia deal by year-end

- Skyworld’s Bennington Residences transforming Setapak

- KSK Land ups the ante with iconic 8 Conlay

- Hua Yang keen to buy more land

- Real estate crowdfunding in Malaysia

- Developer to launch new tower

- Locus @ KLCV coming up in Cheras

- Penduline’s initial 132 homes 85% sold

- Sales gallery of RM5.4bil mixed development 8 Conl...

- KSK raises price of 8 Conlay

- Will slowdown make houses more affordable?

- RM7b Pavilion Damansara project to start in 2Q2016

- Tribunal rules 28 Boulevard soho units GST exempt

- Mah Sing introduces an apartment designed for fami...

- Selayang’s next rising star

- MRCB exploring options to finance new projects

- Hua Yang aborts plan to buy Penang land due to SPA...

- Developer’s new project draws crowd

- IJM Land offers affordably priced homes in Bandar ...

- KSK Land’s 8 Conlay to launch first residence towe...

- Developer launches final phase

- Sunway Velocity 40% completed

- New addition to KL’s skyline

- Secondary property sales may take lead in Malaysia

- 1MDB Real Estate gets 2 final bids for sale in Ban...

- AZRB, Getrahome secure two Kwasa Damansara projects

- Developer to build alternative access routes to PJU10

- SP Setia to launch RM500mil worth of apartments in...

- Govt to expand use of IBS to lower prices of houses

- Overwhelming response to service apartments in Klang

- Call to gate up neighbourhood

- Tycoon land sales raise questions

- Public rail transport to boost Sunway Velocity

- Singaporeans like landed properties in Iskandar, s...

- IOI project in Sepang draws much interest

- Milux makes foray into property development

- New rules on transit-oriented development

- All about buying houses in Klang

- Ahmad Zaki unit wins PJ project with GDV of RM257mil

- Plenitude maintains sales target

- AZRB to jointly develop RM257mil GDV project in Kw...

- MRCB land strategy, eyes Bukit Jalil deal

- ▼ November (57)